Although we haven't added to our gold position in some months at Investophoria, it's still fun to watch.

Gold Bugs are one-of-a-kind type people. When they are right, they are right. When they are wrong, they

will be right. And here's the funny thing. Although most of the outside investing world goes through periods of scoffing (think late 1990's to early 2000's), to periods where telling someone "gold is going down" gets you looked at like you are some amorphous blob of alien goo that ejected itself from a UFO exhaust, they hold true to their gold-buggery through the high times and the low times. Gold bugs are one of the rare breed of individual who never lets go.

However, a true bug is even rarer than an "average" gold bug - the actual ranks of gold buggery swell and subside, like the tide of a sunset ocean.

The true gold bug does not care so much about the price of gold as the idea of gold itself.

Gold truly is a remarkable metal. It is the singular item that above all others has been naturally chosen by the markets to facilitate trade and store value.

Gold bugs understand this, and wait for the day that the wide-spread use of this universal medium returns. The days where the philosophy of gold and the true economic freedom of gold are recognized by the majority, instead of a small minority.

What is this freedom? What is this philosophy? Why the heck do gold bugs get so damned buggish about the yellow metal?

In order to capture the truth of gold, I would need weeks of writing to list its virtues and strengths. However I do not have weeks to write this article just as you don't have weeks to read it. So I'll instead refer you to the folks who have paved the way. Here's a good place for you to start:

Human Action by Ludwig Von Mises - You can Read it Here for Free!

Gold and Economic Freedom - By Alan Greenspan, before "the fall".

Right now, gold bugs true and "en-vogue" are loudly proclaiming victory as gold has YET AGAIN made a new record high. At long last they are vindicated! At long last all those who scoffed at them since the early 1980's are proven wrong!

But the point of the matter is that gold bugs have in fact NOT been proven right, and the scoffers are probably going to get one last chance to scoff.

At least, Not Yet.

Do you remember the post-dot-com-bubble recession? Hardly, I know - it was merely a blip a notch between two giant waves of economic growth. Few people remember why the activities of government and Federal Reserve alike were so dangerous, and one of the specific reasons that we saw the greatest credit fueled housing bubble in the history of recorded mankind.

So, why did every average person, every newscaster, every mainstream investment adviser all stampede toward real estate like a a herd of antelope running from a pride of ravenous lions?

It's pretty simple. So much easy money was injected, such a tidal wave of cheap dollar credit was flooded into the economy at the first

signs of recession, that

housing starts did not go down at all during the recession.

In fact, they increased.

The significance of this was immense. This was the first recorded recession in American history where housing starts did not decline. The first time that house prices didn't suffer.

Never mind the cause, the disease, people looked at the symptoms - the result. They forgot all past recessions and focused on this singular and momentous even in economic history. The soon-to-be-mantra, chanted by one and all and a contrarian's ultimate red-flag bubble-warning:

Houses don't go down in value. They are recession proof. They are an investment. You can't lose money in real estate.

And so on

Here we are today. Even without knowing what I know about price movements, about bubbles, about unwinding long-term false price-signals, the contrarian in me tells me there is some time to go. Even without knowing that whenever a massive psychological bubble is created, so much malinvestment exists in that bubble that the end result is a LOWER measure of success (price) than before the bubble was created.

Because everyone out there is still calling for "a bottom in real estate." They have been calling for it since the first "correction" in prices. Real estate is some ways off from being cheap, folks. The time to buy a house is when everyone complains that money

cannot be made in real estate, and that you are crazy and will lose your shirt if you invest in it. We are far from that point. We need the

philosophy of real estate to change.

Which brings me back to gold - why gold bugs are going to have to wait some time longer to feel vindicated and victorious. To feel that the stripes they earned slowly accumulating their real wealth have paid off.

The philosophy of gold is not mainstream. The fact that it was the best-performing "asset" during the stock market crash, the real estate crash, the bond market crash, the commodity crash, all of it.

The same situation that occurred with real estate in 2002 has occurred with gold. People don't buy it as money, they don't save and store wealth with it, they are seeking capital gains.

And when the majority is seeking capital gains (just look at paper-holding ETF inflows and Commitment of Traders reports for gold investment to verify what I'm talking about here), not-to-far-away comes the point where they lose. The nominal value of their investments decline.

Gold just smashed through a record with a breathtaking rally. It's holding up at $1090.00 as I write this. Gold bugs are celebrating again.

But they should remember. When they were buying gold, it was contrarian. In 2002, at $250 an ounce, when the last Wall Street analyst simply gave up on covering gold, saying "there is nothing good about gold", that was the time to buy.

But now the "never-go-down" psychology of mainstream investors has permeated into gold. Buying gold is so

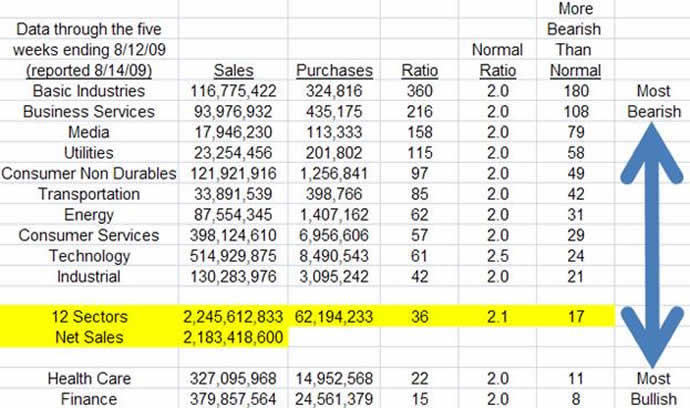

in right now, that even high-end retailers are selling bars out of their storefronts. To the contrarian in me, this signals an imminent top. This is the stage where "hope" has taken over in the place of "worry", which is where real rally build. I would be remiss to pick an absolute top, but in reading the daily COT report, the maximum extension of gold buyers vs. sellers that has been the theme of the last 4 weeks seems over-extended at best.

Gold's young cousin, silver, has still failed to make a new high with gold. Far from it. If this were a true new high, silver should be somewhere about $23-$25 per ounce. However it is far from it, having failed to even breach the $18 mark today.

Gold is going to suffer a serious correction in dollar terms. Greater than the one that occurred last fall, as this positive sentiment must be wound out. Dare I call these new highs in gold "malinvestment" as I would real estate? I certainly will, though even I cringe as I type the word. Malinvestment has to do with expectation and intent - those buying gold now have the same expectations of gold they did of real estate in 2006, that it will continue to go up.

But the philosophy has not changed. No, dear readers, the REAL future move in gold will be one where the everyman and every-woman is awakened to its virtues. The speculators will have moved on to some other asset class, some other investment. They will be too "worried" about gold's price to bother trying a second go. This is where gold will finally see its real glory and climb the long and arduous "wall of worry". Once the philosophy changes, so shall vindication of gold-bugs be realized. Gold will quietly cross the $1100, $1200, $1300 and so-on mark while the very few are watching.

Real bull markets do not occur in the spotlight. Tops do. And bottoms.

The US dollar is possibly the most hated piece of paper in investor terms on earth today (leaving aside notable exceptions such as Zimbabwe's dollar et al hyperinflationist currencies). Gold is the most loved metal. That is why we fly the contrarian flag today. The deflationist flag.

But we will be watching our dear metals. I am no gold-bull, but a gold-bug. And when gold really IS the best store of value you can bet the farm that I will be a buyer. Today, though, it is not - too many speculators have sucked the value out of it. Once they are gone my bull-flag will be back up, and up long-term.

Until then, stay the course and protect your hard-earned savings, dear readers. The time to be bullish on the metals is not far at hand. It is just not today.

Happy Investing All.

Derek.

.

As more debt defaults are called in, the demand for USD's - which make up a huge majority of all debt in the world - will continuously grow, fueling even further increases in its value due to the actual scarcity of cash reserves relative to debt, which is currently treated as cash in most markets.

As more debt defaults are called in, the demand for USD's - which make up a huge majority of all debt in the world - will continuously grow, fueling even further increases in its value due to the actual scarcity of cash reserves relative to debt, which is currently treated as cash in most markets.

{kind=link}